Page 14 - Azerbaijan State University of Economics

P. 14

THE JOURNAL OF ECONOMIC SCIENCES: THEORY AND PRACTICE, V.78, # 1, 2021, pp. 4-25

The key elements of this calculation are the number of students taught in the school

unit, salary regulation and the coefficient that can be interpreted as the major

determinant of funding is the number of students in the school. The amount needed

to cover teacher and other staff salaries per a school unit was calculated on the base

of the average salary for 12 months. This amount forms the core of the student

basket. This was given as a fixed amount of annual salary limit (SL) for a school

unit in each budget year counted on the principle of the formula that took into

consideration number of teaching (NTS) and non-teaching staff (NNTS) multiplied

by the average salary of teaching (AST) and non-teaching staff (ASNT):

SL =12 x (NTS x AST + NNTS x ASNT)

The grant is calculated as a fixed per-student amount. NTS and NNTS were given by

a performance – coefficient ratio that calculated with a given number of students in

total per a school unit (P) and coefficients for the teaching (CftT) respectively non-

teaching staff (CftNT):

NTS = P/CftT NTS = P/CftNT

As already mentioned the key component of the system that was crucial was the

number of students officially attending the school. Other decisions made by the

schools were not affected directly by any single component of the formula or the

method of calculation, only through the amount of the student basket. This is given

as a fixed amount in each budget year and the budget or other decisions made by the

municipalities or schools were not affected directly. The CftT / CFtNT, AST /

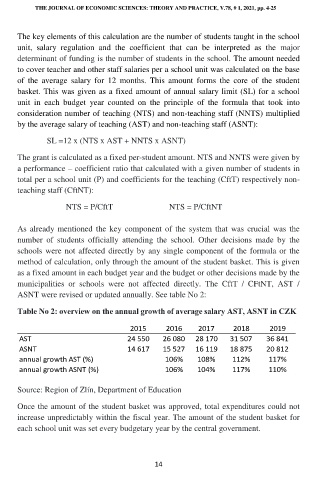

ASNT were revised or updated annually. See table No 2:

Table No 2: overview on the annual growth of average salary AST, ASNT in CZK

2015 2016 2017 2018 2019

AST 24 550 26 080 28 170 31 507 36 841

ASNT 14 617 15 527 16 119 18 875 20 812

annual growth AST (%) 106% 108% 112% 117%

annual growth ASNT (%) 106% 104% 117% 110%

Source: Region of Zlín, Department of Education

Once the amount of the student basket was approved, total expenditures could not

increase unpredictably within the fiscal year. The amount of the student basket for

each school unit was set every budgetary year by the central government.

14