Page 30 - Azerbaijan State University of Economics

P. 30

Gorkhmaz Imanov, Ali Ahmadov: Estimation of the Optimal Size of Financial Depth

in Terms of Macro-Stability

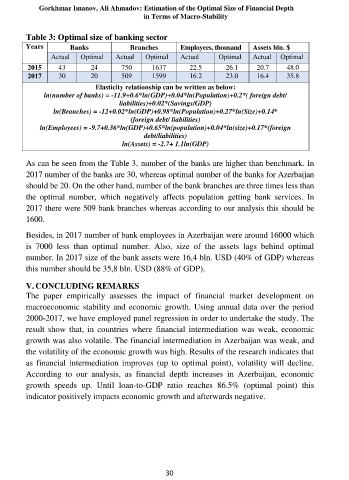

Table 3: Optimal size of banking sector

Years Banks Branches Employees, thousand Assets bln. $

Actual Optimal Actual Optimal Actual Optimal Actual Optimal

2015 43 24 750 1637 22.5 26.1 20.7 48.0

2017 30 20 509 1599 16.2 23.0 16.4 35.8

Elasticity relationship can be written as below:

ln(number of banks) = -11.9+0.6*ln(GDP)+0.04*ln(Population)+0.2*( foreign debt/

liabilities)+0.02*(Savings/GDP)

ln(Branches) = -12+0.02*ln(GDP)+0.98*ln(Population)+0.27*ln(Size)+0.14*

(foreign debt/ liabilities)

ln(Employees) = -9.7+0.36*ln(GDP)+0.65*ln(population)+0.04*ln(size)+0.17*(foreign

debt/liabilities)

ln(Assets) = -2.7+ 1.1ln(GDP)

As can be seen from the Table 3, number of the banks are higher than benchmark. In

2017 number of the banks are 30, whereas optimal number of the banks for Azerbaijan

should be 20. On the other hand, number of the bank branches are three times less than

the optimal number, which negatively affects population getting bank services. In

2017 there were 509 bank branches whereas according to our analysis this should be

1600.

Besides, in 2017 number of bank employees in Azerbaijan were around 16000 which

is 7000 less than optimal number. Also, size of the assets lags behind optimal

number. In 2017 size of the bank assets were 16,4 bln. USD (40% of GDP) whereas

this number should be 35,8 bln. USD (88% of GDP).

V. CONCLUDING REMARKS

The paper empirically assesses the impact of financial market development on

macroeconomic stability and economic growth. Using annual data over the period

2000-2017, we have employed panel regression in order to undertake the study. The

result show that, in countries where financial intermediation was weak, economic

growth was also volatile. The financial intermediation in Azerbaijan was weak, and

the volatility of the economic growth was high. Results of the research indicates that

as financial intermediation improves (up to optimal point), volatility will decline.

According to our analysis, as financial depth increases in Azerbaijan, economic

growth speeds up. Until loan-to-GDP ratio reaches 86.5% (optimal point) this

indicator positively impacts economic growth and afterwards negative.

30