Page 76 - Azerbaijan State University of Economics

P. 76

THE JOURNAL OF ECONOMIC SCIENCES: THEORY AND PRACTICE, V.71, # 2, 2014, pp. 66-80

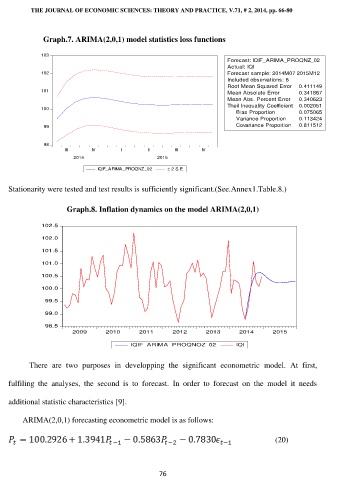

Graph.7. ARIMA(2,0,1) model statistics loss functions

103

Forecast: IQIF_ARIMA_PROQNZ_02

Actual: IQI

102 Forecast sample: 2014M07 2015M12

Included observations: 6

Root Mean Squared Error 0.411149

101 Mean Absolute Error 0.341867

Mean Abs. Percent Error 0.340623

Theil Inequality Coefficient 0.002051

100

Bias Proportion 0.075065

Variance Proportion 0.113424

99 Covariance Proportion 0.811512

98

III IV I II III IV

2014 2015

IQIF_ARIMA_PROQNZ_02 ± 2 S.E.

Stationarity were tested and test results is sufficiently significant.(See.Annex1.Table.8.)

Graph.8. Inflation dynamics on the model ARIMA(2,0,1)

102.5

102.0

101.5

101.0

100.5

100.0

99.5

99.0

98.5

2009 2010 2011 2012 2013 2014 2015

IQIF_ARIMA_PROQNOZ_02 IQI

There are two purposes in developping the significant econometric model. At first,

fulfiling the analyses, the second is to forecast. In order to forecast on the model it needs

additional statistic characteristics [9].

ARIMA(2,0,1) forecasting econometric model is as follows:

(20)

76