Page 99 - Azerbaijan State University of Economics

P. 99

THE JOURNAL OF ECONOMIC SCIENCES: THEORY AND PRACTICE, V.72, # 1, 2015, pp. 95-102

possible, and we should continue with caution toward the regression outcome and

try to improve the regression so that we can rule out autocorrelation.

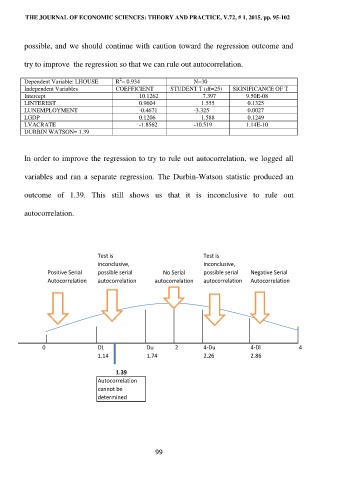

2

Dependent Variable: LHOUSE R = 0.934 N=30

Independent Variables COEFFICIENT STUDENT T (df=25) SIGNIFICANCE OF T

Intercept 10.1262 7.397 9.50E-08

LINTEREST 0.9604 1.555 0.1325

LUNEMPLOYMENT -0.4671 -3.325 0.0027

LGDP 0.1206 1.588 0.1249

LVACRATE -1.8562 -10.519 1.14E-10

DURBIN WATSON= 1.39

In order to improve the regression to try to rule out autocorrelation, we logged all

variables and ran a separate regression. The Durbin-Watson statistic produced an

outcome of 1.39. This still shows us that it is inconclusive to rule out

autocorrelation.

Test is Test is

inconclusive, inconclusive,

Positive Serial possible serial No Serial possible serial Negative Serial

Autocorrelation autocorrelation autocorrelation autocorrelation Autocorrelation

0 DL Du 2 4-Du 4-Dl 4

1.14 1.74 2.26 2.86

1.39

Autocorrelation

cannot be

determined

99