Page 42 - Azerbaijan State University of Economics

P. 42

Turaj Musayev: The Oil Boom in Azerbaijan and Modeling of Economic Growth in Post-Oil Era

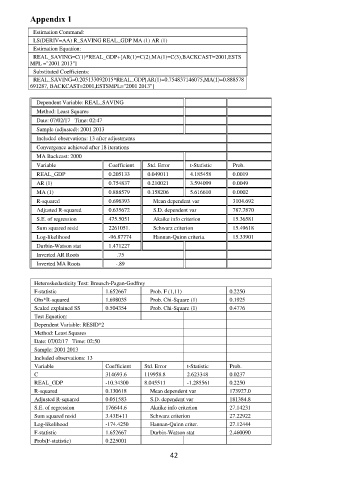

Appendıx 1

Estimation Command:

LS(DERIV=AA) R_SAVING REAL_GDP MA (1) AR (1)

Estimation Equation:

REAL_SAVING=C(1)*REAL_GDP+[AR(1)=C(2),MA(1)=C(3),BACKCAST=2001,ESTS

MPL ="2001 2013"]

Substituted Coefficients:

REAL_SAVING=0.205133092015*REAL_GDP[AR(1)=0.754837146075,MA(1)=0.888578

691287, BACKCAST=2001,ESTSMPL="2001 2013"]

Dependent Variable: REAL_SAVING

Method: Least Squares

Date: 07/02/17 Time: 02:47

Sample (adjusted): 2001 2013

Included observations: 13 after adjustments

Convergence achieved after 18 iterations

MA Backcast: 2000

Variable Coefficient Std. Error t-Statistic Prob.

REAL_GDP 0.205133 0.049011 4.185458 0.0019

AR (1) 0.754837 0.210021 3.594099 0.0049

MA (1) 0.888579 0.158206 5.616610 0.0002

R-squared 0.696393 Mean dependent var 3104.692

Adjusted R-squared 0.635672 S.D. dependent var 787.7870

S.E. of regression 475.5051 Akaike info criterion 15.36581

Sum squared resid 2261051. Schwarz criterion 15.49618

Log-likelihood -96.87774 Hannan-Quinn criteria. 15.33901

Durbin-Watson stat 1.471227

Inverted AR Roots .75

Inverted MA Roots -.89

Heteroskedasticity Test: Breusch-Pagan-Godfrey

F-statistic 1.652667 Prob. F (1,11) 0.2250

Obs*R-squared 1.698035 Prob. Chi-Square (1) 0.1925

Scaled explained SS 0.504354 Prob. Chi-Square (1) 0.4776

Test Equation:

Dependent Variable: RESID^2

Method: Least Squares

Date: 07/02/17 Time: 02:50

Sample: 2001 2013

Included observations: 13

Variable Coefficient Std. Error t-Statistic Prob.

C 314693.6 119958.8 2.623348 0.0237

REAL_GDP -10.34300 8.045511 -1.285561 0.2250

R-squared 0.130618 Mean dependent var 173927.0

Adjusted R-squared 0.051583 S.D. dependent var 181384.8

S.E. of regression 176644.6 Akaike info criterion 27.14231

Sum squared resid 3.43E+11 Schwarz criterion 27.22922

Log-likelihood -174.4250 Hannan-Quinn criter. 27.12444

F-statistic 1.652667 Durbin-Watson stat 2.460090

Prob(F-statistic) 0.225001

42